Market moves across the month were to the south. Fixed income markets seemed to have a more drastic message on the monitor than that of equities.

Fixed Income: 2-Yr Treas Yield 4.16% | 10-Yr Treas. Yield 4.28%

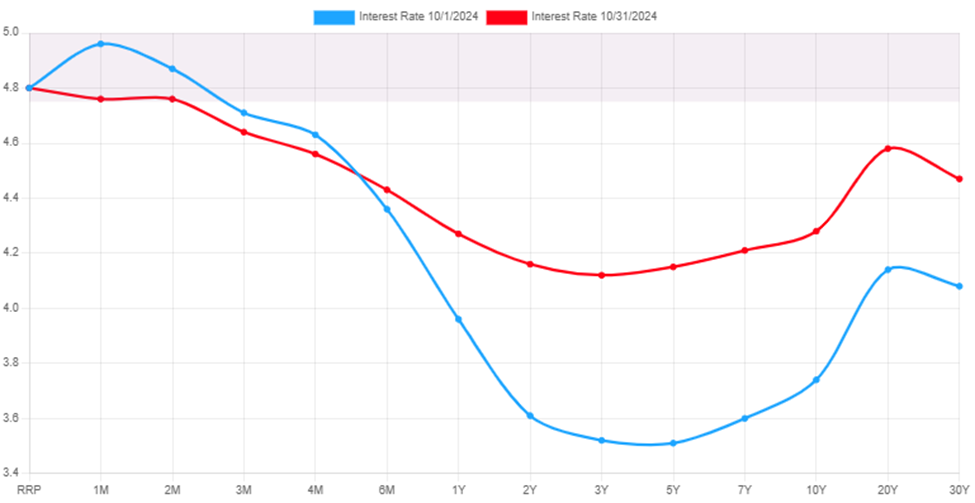

Bond markets went for a reversal ride in October. After several months of falling rates, we began to see a pullback in the bond market as interest rates rose. The 2-year treasury rose 0.55%, while the 10-year treasury rose 0.54%. The good news is that while rising, the rates did not invert again. The long picture remains intact. We are still in an elevated rate environment with them more likely to drift south rather than north. This move may have been the result of predictions for a potential structure that would mean tariffs. This would reflect a higher inflation potential which would signal a slower path in future rate cuts. Additional good news is that while rates from 6 months on rose, shorter duration rates continued to fall. This bodes well for the normalization of the entire curve.

Equities: Dow Jones 1.34% | S&P 500 0.99% | NASDAQ 0.52%

While it was a down month for equites, the overall move south was not bad for the month. From the top of the market for the S&P 500 (10/18/2024) to the end of the month logged a 2.83%. This proved to be a mild lead up to the beginning of November. The nice part is that while a correction has not materialized, earnings season did, bringing the P/E ratio for the S&P 500 back down to 21.19.

Throughout the month utility stock did well until the last week of the month. A shifting towards Financial and consumer discretionary was underway. Neither of which are surprising given interest rates (favoring financials) and the fact that we are in the fourth quarter… I like to say, ‘Americans spend money they do not have on things they do not need’, AKA: holiday season!

Conclusion

Equities pulled back less than was indicative of the rate move on the bond market. The move there signaled more concern about higher rates for longer than equities chose to price in. The shift in rates seemed like a long-term change in projection, while short rates seemed anchored to FRB actions. The longer rage rates often can be equated to long range GDP expectations. If the view is that we would have stronger forward GDP in 5 years, then we see a stronger 5-year rate.

A Look Ahead…

Market responses in October could have been far more drastic than they were. We should feel fortunate that we got the October that we did. This still leaves a correction (a market fall of 10% to 19%) unattended to. The last one ended 10/27/2023. While stretched P/E’s from over the summer have become more reasonable, that’s been due to strong earnings. Those may continue in the short run, but moving into 2025 those might be harder to come by. It may very well cause a correction in the first half of the year.

~ Your Future… Our Services… Together! ~

Your interest in our articles helps us reach more people. To show your appreciation for this post, please “like” the article on one of the links below:

FOR MORE INFORMATION:

If you would like to receive this weekly article and other timely information follow us, here.

Always remember that while this is a week in review, this does not trigger or relate to trading activity on your account with Financial Future Services. Broad diversification across several asset classes with a long-term holding strategy is the best strategy in any market environment.

Any and all third-party posts or responses to this blog do not reflect the views of the firm and have not been reviewed by the firm for completeness or accuracy.

The Federal Reserve is telegraphing their moves. Does this put a target on the back of markets?

Monday

Markets opened the week in the green. The S&P 500 continued from Fridays gains and rose 0.85% on the day. This was in spite of softening PMI data. Specifically concerning was the fall in services data as that makes up the majority of economic activity in the US. The fall, however, was to a level that is still expansionary. It just means we should see a lower level of GDP in the 3rd quarter. Good news on the day included a rise in existing home sales, by 120K units for the month.

Tuesday

The S&P 500 rose marginally on Tuesday. Economic data was fairly light and the focus was on Federal Reserve Board (FRB) Chair Powell’s speech coming on Thursday. New home sales did increase from the prior month by 1.0% (July), missing expectations of a 3% increase.

Wednesday

In another muted day of trading, The S&P 500 was up 0.25%. Again, focus intensified on tomorrow’s Jackson Hole Symposium speech by the FRB. Core durable goods orders, a good indicator of future demand, rose 0.7% (July). All week, FRB members have been sounding the call for tapering of the FRB bond buying program. This has kept what would have been a strong week, rather tepid.

Thursday

The S&P 500 fell 0.65% on Thursday. This came as the FRB Chair confirmed concerns regarding tapering. They do intend to begin tapering later this year. Assuming the economy maintains I’s trajectory of growth.

Friday

In a re-occurring theme, the S&P 500 made back all of Thursdays losses and then some on Friday. It rose nearly 1%. Core PCE pricing was released Friday showing that inflation has increased 3.6% YoY (July). The black mark on the day was that consumer sentiment preliminary reports is reading at 70.3. A large drop from last month. This is concerning for future spending expectations.

Conclusion

The S&P 500 rose 1.52% in a week where the FRB confirmed tapering of bond purchases will occur later this year. The telegraphed nature of Chair Powell’s behavior should allow market shocks from FRB activity to remain muted. A major part of his statement was that tapering is contingent on continued economic strength, which appears to be fading. A tightening FRB is unlikely in an environment with waning economic production.

~ Your Future… Our Services… Together! ~

Your interest in our articles helps us reach more people. To show your appreciation for this post, please “like” the article on one of the links below:

FOR MORE INFORMATION:

If you would like to receive this weekly article and other timely information follow us, here.

Always remember that while this is a week in review, this does not trigger or relate to trading activity on your account with Financial Future Services. Broad diversification across several asset classes with a long-term holding strategy is the best strategy in any market environment.

Any and all third-party posts or responses to this blog do not reflect the views of the firm and have not been reviewed by the firm for completeness or accuracy.